Global Congress 2023: Trust in the online world will collapse unless there is urgent and dramatic change

The internet has made us more connected than ever before, and new technologies have huge potential to generate positive change for consumers. In finance, digital financial services are giving consumers around the world access to mobile money, in healthcare, AI is set to revolutionise diagnosis processes, and in the marketplace, consumers can experience more personalised shopping experiences,

But new technologies also bring with them a lot of risk, and if we don't approach with caution, trust in the online world will collapse, and consumers may be at risk of harm.

In many places around the world, consumer protection in the digital sphere is lagging behind. Key boxes are not being ticked and trust is lacking across the online marketplace and in areas like Buy Now Pay Later, mobile money, and cryptocurrency.

We are living in a digital world, but relying on rules for an analogue one. Updates and innovations are needed now. Tech like AI and opaque algorithms - used in facial recognition technology and to determine personal loans - have the power to alter the course of people's lives.

This has been a key area of conversation at the Consumers International Global Congress 2023, with speakers in several sessions highlighting not just pressing problems, but also suggesting solutions that can protect consumers while allowing them to benefit from the latest digital developments. Here are some of the highlights:

Connection and collaboration

Consumers International Director General Helena Leurent opened Global Congress 2023 with a call for connection and collaboration. This was echoed by Deputy President of Kenya, Rigathi Gachagua.

"The digital age has brought about unprecedented opportunities, but it also poses new challenges, especially for consumers. Issues such as data privacy, cybersecurity, and fair competition require our collective attention. It is imperative that we work collaboratively to strengthen international standards for consumer protection, ensure consistency across borders and sectors, and develop innovative solutions that safeguard the rights and interests of consumers globally."

The large strides Kenya has taken in advancing consumer protection are one of the reasons Consumers International chose to hold Global Congress there this year. Rules around increased transparency for payments and charges in mobile financial services have benefited over 30 million Kenyans, the Chairman of the Competition Authority of Kenya, Shaka Kariuki, told Congress.

Developments such as this are critical given the rapidly rising use of digital payments not just in Kenya, which has the M-PESA system, but in many other parts of the world as well. Gachagua called for increasing integration of new technologies, including artificial intelligence (AI), to suppress recent rises in consumer exploitation, adding that effective consumer protection mechanisms are the only way to ensure the effective and efficient movement of money across borders.

Consumers play a pivotal role in driving economies and shaping the global marketplace, Gachagua added, so developing stronger protections for people in the digital world will ultimately benefit everyone.

Kariuki said that unified commitments, collaborations and actionable initiatives will shape the future of consumer rights. The Consumers International Global Congress aims to provide a roadmap to help make that happen.

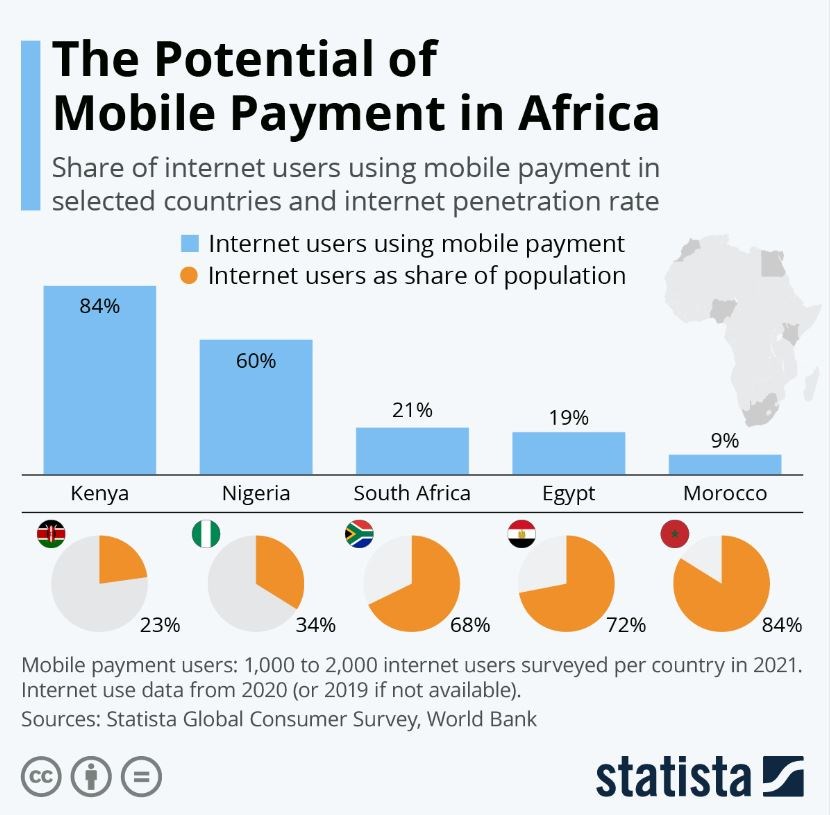

https://www.statista.com/chart/27017/mobile-payment-in-africa/

Adapting to AI

Ai could dramatically change the way businesses interact with consumers. Ensuring this change benefits consumers was the focus of The impact of generative AI on consumers.

AI could lead to a powerful wave of dis-and mis-information. Over half of consumers are unable to accurately distinguish between human-made and AI content. Panellists highlighted the importance of instating consumer-led regulation of generative AI, especially when it comes to ethical standards. Their recommendations include clear guidelines and ensuring human intervention is standard in AI development.

Being alert to ethics washing is critical, said Gilly Wong, Chief Executive of Hong Kong Consumer Council, who said some corporations may try to downplay the potential impact of AI in this area.

The call for genuine ethical considerations in AI development and regulation is vital, said Wong, and transparency and accountability is essential to ensure ethical standards aren't mere window dressing.

Wong – along with Rebecca Kelly Slaughter, Commissioner at the US Federal Trade Commission – also called for collaboration on a global approach to AI regulation, saying this is the only effective way to truly address misinformation, scams and other ethical concerns.

While praising the EU's AI Act and UNESCO's AI framework, Wong also said there is a need for a strong national voice to be heard, with consumer organisations ideally placed to take on this critical role. Slaughter described consumer education as the bedrock of AI regulation, saying that a fair yet competitive marketplace cannot exist without it.

The panel also focused on AI’s potential role in Africa’s digital economy, with Melissa Omino, Director of the Centre for Intellectual Property and Information Technology Law at Strathmore University spotlighting the work the African Union is doing on data governance, and suggesting they can provide a blueprint for global AI ethics. Leading organisations such as the Bill & Melinda Gates Foundation have called for a need to ensure AI equity. Deon Woods Bell, Senior Advisor on Global Policy and Advocacy at the Bill & Melinda Gates Foundation, opened the session by pointing towards Gates' principles for inclusive, responsible AI that builds equitable access and does not leave vulnerable populations behind. so that everyone has access to the potential benefits.

One fair and responsible use of AI could be in the development of digital public infrastructure, suggested Deon. The concept is built on principles including using networked open technology standards in the public interest. In reality, that means using digital systems to more efficiently deliver social services and economic opportunities to all citizens. The UN says it could also help countries contribute towards achieving the Sustainable Development Goals.

These issues will all be explored more on World Consumer Rights Day on 15 March 2024, where we have set a theme of “Fair and Responsible AI for Consumers”.

Product safety for online sales

Almost nine in every 10 products that have been banned or recalled are still available in online marketplaces, according to the OECD. A combination of better regulation and voluntary initiatives is needed to stop this happening, according to speakers at Effective Frameworks for Product Safety.

The cross-border nature of e-commerce is a source of some of these problems, so cross-border collaboration on international rules is needed to resolve this. In a marketplace with no physical boundaries, setting regulatory boundaries to protect consumers is absolutely imperative, according to Rosemary Shumirayi Chikarakara Mpofu, Chief Executive Officer and Executive Director of the Consumer Council of Zimbabwe.

Any rules must include clear guidance on where responsibilities and liabilities lie, and facilitate better data sharing to help enforce product bans, the panellists suggested. But maintaining the ability to flex and adapt as the online world changes is also needed, added Rainer Ettel, Germany’s Head of Directorate for Cross-Sectoral Consumer Policy Issues.

Driving change in digital finance

Two-thirds of the African population do not have a bank account, but instead prefer to keep their money in a box or under their mattress, payment provider AfricaNenda’s Chief Executive Officer, Robert Ochola, told the Channels of Change Towards Fair Digital Finance session.

Innovative finance models have the potential to rapidly expand access, choice and transparency for unbanked consumers around the world, but in a world where 68% of people don’t trust companies to protect their data, the digital finance sector has to prove its principles, not just its practicality.

This is why Consumers International launched a new multi-stakeholder initiative; Building the Consumer Voice into Digital Finance. Unveiled by Shamina Singh and supported by Mastercard Center for Inclusive Growth, the initiative will explore models of digital finance that improve consumer protection, elevate the voice of vulnerable consumers, and take learnings from individual economies and look to disseminate them worldwide.

One example of national actions that should be applied globally was provided by panellist Seema Nareeta Shandil, Chief Executive Officer of the Consumer Council of Fiji. Her organisation has gathered insights on consumer needs in the digital world and used this evidence to persuade the government to set up a multi-agency task force to tackle scams.

Singh flagged how a lack of comprehensive data protection laws are putting consumers at risk, and Agustín Reyna, the Director of Legal and Economic Affairs at the Bureau Européen de Unions de Consommateurs, called for global benchmarking on data regulation to help countries put in place robust and progressive legislation.

Examples of progressive work on consumer protection in digital finance were spotlighted in a side event, Engaging the Consumer Voice in Digital Finance. Several grantees of the Consumers International Fair Digital Finance Accelerator were called upon to share their stories. The National Federation of Consumer Assoications of Ivory Coast, which is creating an online complaints resolution system to capture the challenges people are facing in digital finance. Kenya Consumer Organisation and Youth Education Network (Kenya), working in partnership, discussed how they have led the establishment of a set of transparency guidelines to steer discussions with mobile money service providers and regulators.

The Fair Digital Finance Accelerator – funded by the Bill & Melinda Gates Foundation, with support from the Consultative Group to Assist the Poor (CGAP) – now has 65 members from low and middle-income countries working alongside policy-makers to create more effective regulation and resolution mechanisms. Consumer financial protection frameworks are improving as a result, Christine Hougaard, Technical Director of African economic impact agency Cenfri, told delegates. However, things are far from perfect, and if consumers – especially the most vulnerable ones – continue to pay the price, this jeopardises trust in the entire digital finance system.

Dealing with data

Data was also the focus of the session Around the World in 80 Bytes: Building Privacy and Redress into Cross-border Data Flows. Unclear data usage by companies, invasive data collection and the risks associated with "click to consent" practices came under the microscope, as speakers from companies including Mozilla and Visa called for moves to empower consumers so they can better understand and control their personal data. This is a responsibility for companies and governments, not a choice, they added.

There is also a clear need for the harmonisation of data governance frameworks globally and greater transparency in trade agreements, panellists said, given that current free flows of data across borders often leave consumers without effective means to enforce their rights. Collaboration has to be the cornerstone of responsible data governance, with shared values as the only way to build up trust in the interconnected online world, delegates heard.

Regulatory gaps have been exposed by a case in Kenya against cryptocurrency company Worldcoin for its handling of data, panellists said, adding that this shows a clear need for far more robust rules on data protection and privacy. Setting up the right safeguards will require input from policymakers, industry leaders and consumer advocates, delegates heard.

Consumers International’s newly launched Interoperability for all: Cross-border consumer redress and trust initiative can help guide these discussions. At its heart will be considerations around the people affected by data transfers, including how their rights can be upheld and how they can get access to redress if required. Its ultimate goal is to turn abstract principles into real-world consumer protection.

Building consumer literacy in mobile money

There are 1.2 billion registered mobile money accounts worldwide, giving people access to easier ways to send and receive money, build savings and access social supports. But a lack of consumer literacy means these accounts are not always working as well for consumers as they could be, panellists said in the Redefining Consumer Journeys in Mobile Money session.

This lack of literacy is creating risks around fraud and digital consumer credits, and is leaving people with financial losses as a result. This has happened to 14% of users in Nigeria, while a third of users in Uganda have had to pay extra on transactions, according to an Innovations for Poverty Action survey.

Technology should also be used to help protect people, panellists said, describing a need for the market to be “inherently innovative” to safeguard consumers. This is already happening in Uganda, where the Regenerative Voice project is harnessing machine learning to identify fraudulent apps on the Google Play Store.

There is a wider need to “cultivate a quality culture”, delegates heard, with recommendations including setting up partnerships to collect consumer complaints, and shifting away from a “sandbox” environment within the industry to one where companies open dialogues and support one another in building better products and experiences to instil consumer confidence.

Tackling scams

More than $1 trillion has been lost to scams worldwide, and fewer than 10% of victims ever manage to recover what has been stolen from them. Consumers clearly need better protection, but 4 in 10 countries still do not have consumer protection laws covering the online marketplace.

Digital platforms need to bear much more responsibility for this, and they should face heavy penalties if they fail to act, panellists said during the Scams, Fraud and Fake Reviews: Building Trust in the Digital Economy session. Scammers are making huge amounts of money from vulnerable people, but online platforms, banks and telephone companies are also benefitting from the drive towards digital, so there needs to be a degree of accountability with this level of profitability, said Consumer NZ’s Chief Executive Officer, Jon Duffy.

Mozilla Africa's Head of Product Innovation, Patrick Sambao, backed this up by noting that as online platforms are the door to the internet, they have a duty to ensure consumers are safe. They should be working to spot potential scammers early and block access for these criminals. The panel were in support, suggesting that increased international collaboration and information sharing is crucial to make this happen.

The session included the launch of Consumers International's Global Statement to Stop Online Scams which calls on governments to require online platforms to take effective action in the prevention, detection and disruption of scams. Over 20 consumer organisations worldwide have lent their support to the statement.

Honesty around algorithms

The use of algorithms is on the rise in all areas of life, from insurance and loan approvals to job applications. AI is only expected to accelerate this trend, and while automated algorithms can speed up processes for companies, work needs to be done to ensure they also have the interests of consumers at their heart.

Algorithmic bias was one of the key issues flagged during the Achieving Fair and Transparent Algorithms for Consumers session. Transparency around when and how algorithms are being used is needed, according to Mastercard’s Vice President of Global Public Policy, Heba Shams, who said that companies know what information is going into their “black box” and they have to be honest about this with consumers.

Companies need to stop and think about the trade-off between convenience and security, particularly when algorithms are being used with financial data, the panel said. Mastercard has developed an internal governance framework for AI with principles on data ownership, security, integrity, accountability and transparency, and Spanish consumer federation CECU’s Director, David Sanchez, said more consumer advocacy is needed to shape broader national and international frameworks that prioritise consumer safety, transparency and access to information.

Effective governance must ensure data science is on the side of consumers, DataKind Chief Executive Officer Lauren Woodman said, while Mastercard’s VP Shams called for consensus around “human-centric objectives” in the use of algorithms.